The Pending Recovery of the Discretionary Consumer sector

‘It’s tough to make predictions, especially about the future.’

– Yogi Berra

During my career, I’ve experienced five material downturns in the economy and capital markets. In the early stages of each cycle, valuations of publicly owned Discretionary Consumer (“DC”) ** companies led other sectors down as economic headwinds intensified. Once the Fed and Congress initiated stimulus by increasing market liquidity, lowering interest rates, cutting personal and corporate tax rates (or all the foregoing), the DC Index valuation was the first to climb, and more often than not, was the fastest to recover to pre-downturn levels. At the depths of the downturn, the number of negative data points affecting DC businesses far outweighed any positive metrics. Yet the DC sector has come back, frequently roaring back, cycle after cycle.

Being an eternal optimist and counting on history to repeat itself, I know the DC sector will recover. While it is difficult to predict “when” the recovery in the DC sector will commence, I’m going to take a shot at it…

A Look Back

First, a review of the Great Recession and the state of U.S. Households and Corporate entities leading to that very dark era in history. According to the US Census Bureau, in 2008, just as the recession commenced, household leverage exceeded 13% of disposable income. Non-Financial corporate entities were significantly levered with interest expense accounting for 4% of revenues, per the Bureau of Economic Analysis.

Today, both Households and Corporate entities have significantly stronger balance sheets, with Household leverage under 10% of disposable income and Non-Financial Corporates’ interest expense accounting for approximately 2% of revenues. All in all, U.S. Households and Corporate entities are better positioned to weather the weak economy. Household and Corporate spending should minimize the depths and durations that the S&P 500 and the DC indices may languish.

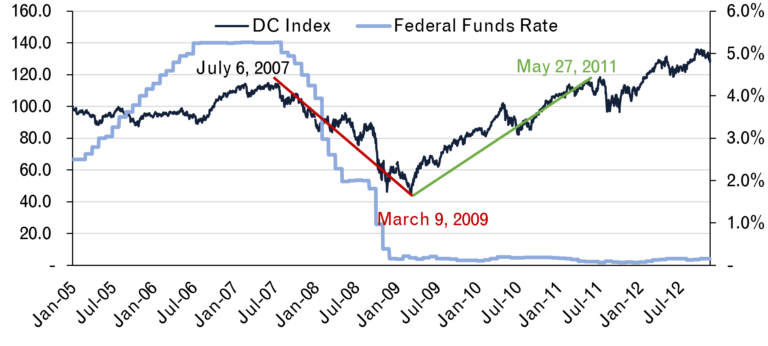

Now, for some charts to illustrate how the DC Index performed before, during and after the Great Recession.

The peak DC Index valuation occurred on July 6, 2007. The DC Index declined by ~60% to its lowest level on March 9, 2009. There was a total of 612 days, or 20.4 months, from the peak to the trough.

In 2008 and 2009, the Fed and Congress took unprecedented steps to resuscitate capital markets and to stimulate the economy. In 2009, the DC Index soared and led to reaching the previous (July ’07) high valuation peak on May 27, 2011, a total of 809 days, or 27 months later.

A Look Ahead

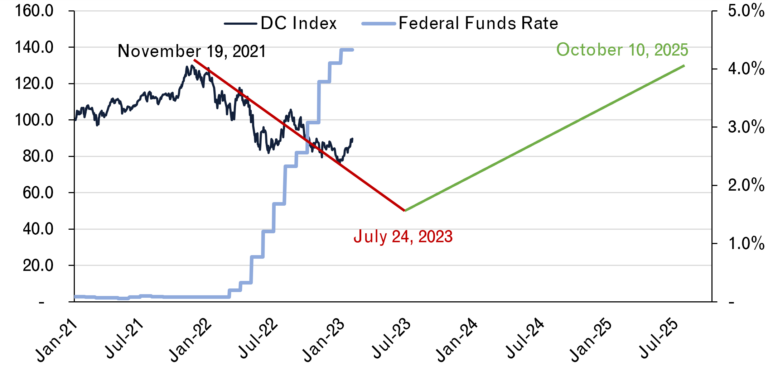

In an effort to forecast the future of the DC Index, I’ll rely on metrics tied to the cycle of the Great Recession. By overlaying the preceding data from 2007 to 2011 to present-day metrics, I’ll provide estimated target dates for the trough and the recovery to the former peak.

The most recent high of the DC Index occurred on November 19, 2021. By overlaying the 20-month historical peak to through, I estimate the DC Index will hit a low in Q3 ’23. Yes, seven to eight months from now, the DC Index will bottom out, then begin its upward momentum.

Now, no recessions are comprised of the same set of variables. One of today’s biggest issues in the DC sector is massive supply chain disruptions. The timeline for resumption of well-oiled supply chains is anyone’s guess. Inflation is another major factor impairing the economy, and the Fed has clearly communicated its intent to battle it with recurring interest rate hikes. I can see how the DC Index low could be pushed out into Q4 ‘23 but I doubt it will occur later than this.

Finally, geo-political risk is the ultimate wildcard. If the U.S. is drawn into a kinetic war with Russia or China, all bets are off. Absent this worst-case scenario, once the vortex is reached, I estimate the DC Index will reach its former November 2021 peak in 27 months, or Q4 ’25.

The storm clouds will break, and sunny days (along with higher DC valuations) will shine upon us. Of this prediction, I believe Yogi would concur.